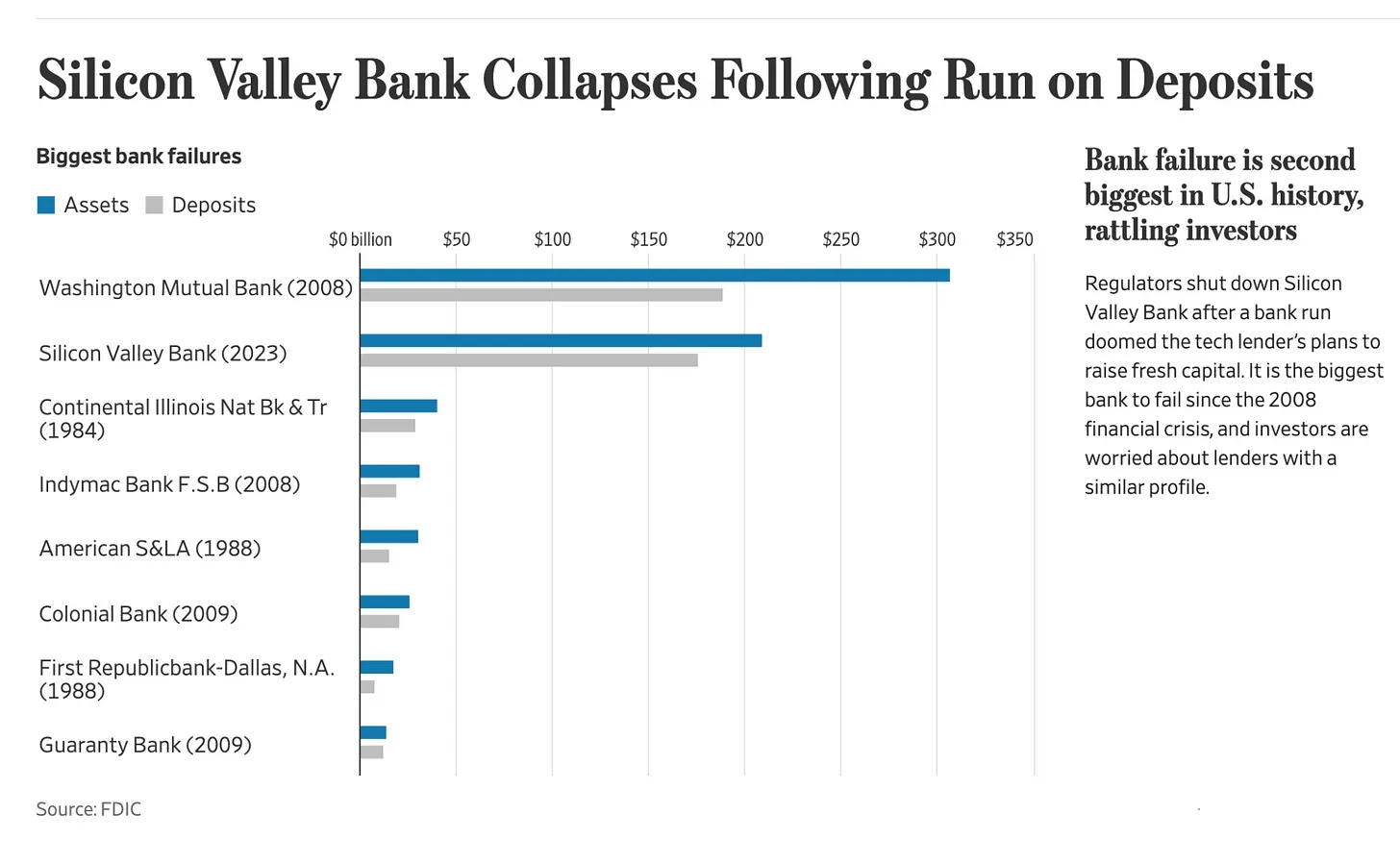

Silicon Valley Bank (SVB) was not a small bank.

It was the 16th largest in US financial system (and there are a lot of banks in the US).

SVB has been around for 40 years and was home to half of all venture-backed startups.

Now it’s the biggest bank failure since 2008 and the second-largest in US history.

Source: Wall St Journal

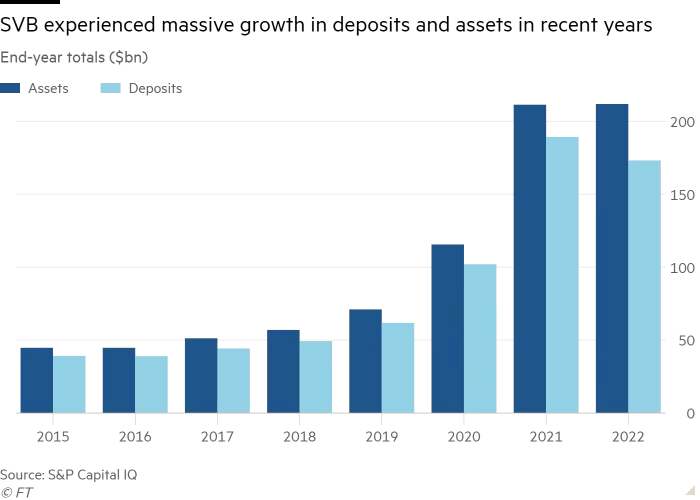

How did this all begin?

SVB received a LOT of deposits from startups. Its deposits tripled from 2018 to 2021.

Source: Financial Times

SVB took these deposits and bought fixed-rate mortgage bonds.

At the peak of the tech investing boom in 2021, customer deposits surged from $102bn to $189bn, leaving the bank awash in “excess liquidity”. At the time, the bank piled much of its customer deposits into long-dated mortgage-backed securities issued by US government agencies, effectively locking away half of its assets for the next decade in safe investments that earn, by today’s standards, little income. – Financial Times

In 2021, SVB bought fixed-rate mortgage bonds.

To be specific, $91 billion was in fixed-rate mortgage bonds carrying an average interest rate of just 1.64 per cent.

In a time when interest rates were low and bond prices were high, SVB’s bonds looked like a safe piggy bank.

But by buying fixed-rate mortgage bonds, they are essentially making a one-way bet on interest rates – that it will stay this low, or that the interest rate hike will be gradual.

Then came 2022, with the Fed started hiking interest rates, and bonds suffered their worst year in history.

Of course, SVB was not the only one in this position. And for that reason, there is a big market in interest rate hedges.

Did SVB have interest rate hedges? No, it didn’t.

By the end of 2022, it only had $563mn worth of hedges left on its books. In comparison, Credit Suisse’s interest rate swap hedges was $135.7bn at the end of 2022.

Panic ensued

In order to cover their losses, in a public release, SVB announced a capital raise.

But they did so without reassuring VCs about the overall strength of their business.

SVB’s CEO told customers to “stay calm,” which is almost guaranteed to increase panic rather than reassure people.

Many VCs told their portfolio companies to pull money out of SVB, and the herd mentality dominated.

The result? The share price of SVB went down the cliff, falling by over 60%.

Looking back, how could SVB have ended up in this exposed position? Why was it not stress-tested?

Because in 2018, the regulations were changed and SVB was leading for the regulations to be lifted.

Some banking experts on Friday pointed out that a bank as large as Silicon Valley Bank might have managed its interest rate risks better had parts of the Dodd-Frank financial-regulatory package, put in place after the 2008 crisis, not been rolled back under President Trump.

In 2018, Mr. Trump signed a bill that lessened regulatory scrutiny for many regional banks. Silicon Valley Bank’s chief executive, Greg Becker, was a strong supporter of the change, which reduced how frequently banks with assets between $100 billion and $250 billion had to submit to stress tests by the Fed.

Source: The New York Times

Fed’s Action

The Federal Deposit Insurance Corporation (FDIC) will pay $250,000 to each depositor no later than Monday.

The Biden administration announced Sunday night that all depositors at the failed Silicon Valley Bank would have access to all their money on Monday morning, approving an extraordinary intervention aimed at averting a crisis in the financial system.

Source: The Washington Post

Final thoughts

A bank run is a symptom of the disease (mismanaged bank risk).

And banks are in the business of trust.

The ultimate victim of this event may be Silicon Valley, not just the bank.